Blog

How to Choose the Right Car for Your Lifestyle and Budget

Buying a car should be simple. Work out what you need, figure out what you can spend, go buy it. Done.

Except it never actually happens that way. You walk into a dealership set on a practical hatchback and somehow end up test-driving a seven-seater SUV with heated everything and a panoramic roof you’ll use twice. The salesperson mentions something about “lifestyle upgrades” and suddenly you’re questioning every decision you’ve ever made.

Having a proper plan helps. First car, tenth car, replacing something held together by rust and sheer determination — the process works the same way.

What Do You Actually Need?

Forget the Instagram fantasy version of your life for a second.

How many people are you realistically carrying around on a regular basis? Not “what if my entire extended family visits” but actual day-to-day use. Are you doing short city runs or grinding out motorway miles? Boot space requirements — work equipment, sports gear, that pushchair that somehow expands to fill any available space?

Someone commuting solo into Birmingham has wildly different needs than a family of five juggling school runs and camping weekends. A builder needs something completely different from a sales rep racking up 30,000 miles annually visiting clients.

City driving usually points toward compact cars or hybrids. Easier parking, cheaper running costs, less aggravation sitting in traffic. Families with kids, dogs, and all the associated chaos tend to appreciate SUV or minivan space. And if you’re towing anything regularly or heading off tarmac, four-wheel drive stops being a nice-to-have.

Budget — The Actual Number, Not the Sticker Price

This trips up most buyers. They see the price on the windscreen and think that’s what cars cost.

It isn’t.

Your real budget needs to include insurance (varies massively by model — that sporty number might cost double to insure), fuel, servicing, road tax, MOT. Financing? Add those monthly payments. Parking permits if you’re in a city. The random repairs that always seem to happen at the worst possible time.

Financial advisors usually recommend keeping total car costs between 15-20% of monthly income. Push beyond that and every unexpected bill stings.

HP finance works well for people who want straightforward ownership. Deposit down, fixed monthly payments, car is yours once you’ve paid it off. No balloon payment surprise at the end, no mileage caps, no handing back keys. You pay, you own. Simple. There’s a reason it’s popular with UK buyers — you know exactly where you stand.

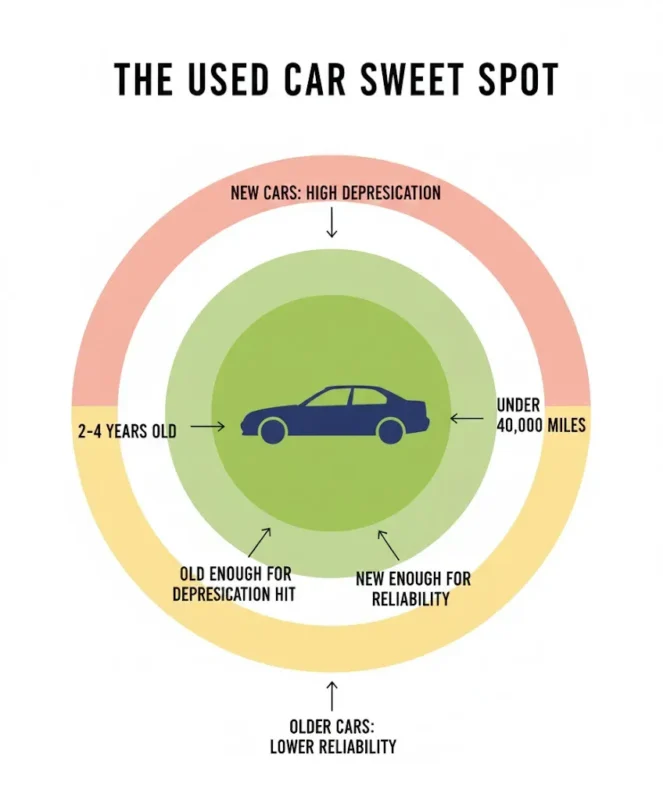

New Cars vs Used: That Depreciation Cliff

New cars smell amazing. Warranty covers everything. Nobody’s been eating crisps between the seats or spilling coffee in places coffee shouldn’t go.

But here’s the brutal bit: 20-30% of the value vanishes the moment you drive off the forecourt. By year three, you’ve lost 40-60%. That’s thousands of pounds evaporating into thin air.

Used cars skip that initial value collapse. A two or three-year-old model with reasonable mileage gets you most of the benefits without the financial punishment.

Certified pre-owned slots in between. Manufacturer-approved, properly inspected, comes with extended warranty. You pay more than private sale prices but you’re buying some peace of mind along with the vehicle.

When does new actually make sense? Planning to keep it 8-10 years. Specific features only available on current models. Manufacturer finance deals that make the maths work out. Outside of those situations? Used wins almost every time, especially if the car’s going to see heavy use anyway.

Different Vehicles, Different Lives

Budget sorted, needs clear — now you can actually look at specific cars.

Hatchbacks remain the sensible urban choice. Affordable, cheap to insure, easy to squeeze into parking spaces that shouldn’t really count as parking spaces. Ford Fiesta, Vauxhall Corsa — they sell by the bucketload for good reason.

Sedans offer more boot space than hatchbacks, quieter motorway cruising, and some people find them more professional-looking if that matters for work. Fair trade-offs.

SUVs have taken over and honestly, it makes sense. Higher driving position, flexible cargo area, feeling of solidity on the road. Running costs are higher though — fuel consumption and insurance both jump up. Crossovers split the difference if you want the look without the full cost hit.

Electric and hybrid options are getting harder to ignore financially. Higher purchase price but significantly cheaper to run, particularly with petrol prices doing what they’re doing. Charging infrastructure keeps expanding — still worth checking what’s actually available near home and work before committing.

Pickups and vans suit specific needs. Hauling equipment and materials regularly? Nothing else really does the job.

Build a shortlist — three to five models — and actually dig into them. Owner reviews on forums, not manufacturer marketing. Real people discussing real problems they’ve had. Much more useful than glossy brochures.

Test Drives: Don’t Skip This

Specifications and photos only tell you so much.

Seats that feel fine for the first five minutes might become uncomfortable after twenty. Driving position might not suit your height or build. Some cars have weirdly placed pedals or steering columns that don’t adjust far enough.

Visibility gets overlooked constantly. Those chunky rear pillars might look sporty but they create blind spots you’ll deal with every single time you reverse or change lanes. Sensors help. They don’t solve the problem entirely.

Test the car in conditions you’ll actually face. Motorway driving planned? Get on the motorway. Tight city streets? Find some tight city streets. Daily stop-start traffic? Sit in some traffic. See how the car actually handles your reality.

Listen for rattles. Feel for vibrations. Notice whether the suspension smooths out bumps or transmits every pothole directly into your spine. Check that the infotainment isn’t infuriating to use while driving — some systems seem designed by people who’ve never actually driven a car.

Bring whoever else will be in the car regularly. Backseat space might work for you but your partner or teenage kids might have opinions. Better to discover those opinions before purchase.

Used Car Checks: Don’t Get Burned

Buying used requires homework. Skip this and you’re gambling.

HPI check first — £10-20 and absolutely essential. Shows outstanding finance, write-off history, whether it’s been reported stolen, mileage discrepancies. Never buy used without one.

Service history tells a story. Regular stamps from decent garages suggest the previous owner actually maintained the thing. Gaps in records should raise eyebrows.

Physical inspection: rust around wheel arches, door sills, underneath the car. Check tyre wear — uneven patterns often mean alignment or suspension problems that’ll cost you later. Start the engine cold and watch the exhaust. Blue smoke means oil burning. White smoke could mean head gasket issues. Neither is good.

Test every electrical component. Windows, locks, air con, heated seats if fitted. These repairs add up fast when something’s not working.

Dashboard warning lights need proper explanation. “Oh that just came on recently” is not an acceptable answer.

Timing Your Purchase

When you buy affects what you pay.

End of month means salespeople chasing targets. They’re often more flexible when they need one more sale for their bonus.

End of quarter amplifies this — March, June, September, December see dealerships pushing harder to shift stock.

Plate change months matter for UK buyers. March and September bring new registrations, so anyone who cares about having the latest plate trades in. Dealerships suddenly have loads of nearly-new stock they need to move. Outgoing models often see decent discounts.

January and February are quieter. Fewer buyers means less competition, more room to negotiate.

Actually Negotiating

Most buyers don’t realise the sticker price is a starting point.

Know market value before walking in. Check Auto Trader, eBay Motors, similar listings from other dealers. This gives you ammunition.

Get quotes from multiple dealers on the same model. Let each one know you’re shopping around. Competition works in your favour.

Don’t fall in love with a specific car during the process. The moment salespeople sense emotional attachment, your negotiating position crumbles. Be genuinely willing to walk away. Often the best deals come via callback when they realise you weren’t bluffing.

Watch for extras bundled in that inflate the price. GAP insurance, paint protection, fabric treatments — some actually have value, others are pure dealer margin. Know what you want before sitting down to discuss add-ons.

Expensive Mistakes to Avoid

Monthly payment obsession. Dealers love stretching loan terms to make expensive cars seem affordable. Lower payment over six years costs far more than higher payment over three years. Total cost matters.

Forgetting insurance research. That sporty model might look affordable until you discover insurance is double the sensible alternative. Get quotes before committing to anything.

Ignoring running costs. Some cars are cheap to buy and expensive to own. German luxury brands often have parts prices that’ll shock you when something breaks.

Skipping MOT history. Government’s free MOT check shows previous test results including advisories. Recurring issues suggest problems nobody bothered fixing properly.

Rushing because of fake urgency. “This offer ends today” almost never actually ends today. Sleep on it. Another car will appear. They always do.

Paperwork You Need

V5C logbook must transfer to your name. Without it, you don’t officially own the vehicle in any meaningful sense.

Valid MOT certificate — check the expiry date so you’re not surprised by needing another test in two weeks.

Full service history with receipts or stamps. Better records mean better resale value later.

Buying from a dealer? Get everything written down. Agreed price, included extras, warranty terms, handover date. Verbal promises mean nothing when disputes happen.

Used cars with outstanding finance need a settlement letter proving the debt is cleared before you complete. Otherwise the finance company can legally repossess what you thought you’d bought.

GAP Insurance: Quick Explanation

Financing a vehicle? GAP insurance covers the gap between what standard insurance pays out (market value when stolen or written off) and what you still owe.

Cars depreciate fast. Yours gets written off in year one, standard insurance might pay £12,000 on a car you still owe £15,000 for. GAP covers that £3,000 difference.

Dealers typically charge much more than buying GAP independently. Shop around before accepting their offer.

Making the Final Call

Pull everything together properly. Compare remaining options across purchase price, running costs, practicality, how they actually felt during test drives, reliability reputation.

HP finance gives you space to make this decision without pressure. Fixed monthly amounts, clear end date, full ownership once you’re done. Straightforward.

The right car fits your actual life now and your realistic plans for the next few years. Not the fantasy version. Not keeping up with what your neighbour drives. Your actual situation, your actual needs.